Imagine a collection of books where each tells a continuous story with the same characters and themes. These books are available in every bookstore or library worldwide, and the story they tell is commonly known.

Now, picture if someone decided to rewrite a passage in one book within their local library. This change would be isolated because every other library and bookstore has the original text.

The altered text in that single book would stick out, unable to blend in unnoticed because it contradicts many unaltered books elsewhere.

Blockchain technology functions in a remarkably similar fashion. It is like a book series for digital information, storing data in 'blocks.'

These blocks are ordered in a 'chain' in every 'library' — or computer — part of the blockchain network.

Any attempt to alter information on one block is immediately apparent when compared to the unaltered blocks on all other computers in the network.

This architecture ensures a high level of security for records, contracts, and any form of data that is significant for private and public transactions. Like the widespread distribution of our hypothetical book series, blockchain's design requires consensus for any change.

Only when every participant agrees can a new 'edition' — or block of data — be added to the chain.

This results in a robust and transparent system where tampering is not just tricky, it's easily detectable, making blockchain a reliable guardian of digital information.

How does a blockchain work?

Delving into how a blockchain functions unveils a confluence of pioneering core technologies that create an innovative system. Below is a closer look at these technologies and their synergy.

Furthermore, for organizations aiming to harness the power of blockchain, professional Blockchain Development Services are available to tailor these technologies to meet specific business needs.

A blockchain works through a combination of several core technologies:

Distributed Ledger Technology (DLT)

This is a sophisticated system where every network member has an entry to the distributed ledger technology, which acts as an authoritative registry of all transactions.

This ledger's design ensures that each transaction is entered just once. This streamlines the process by avoiding the redundant tasks often seen in conventional business networks.

Immutable Records

Once a transaction is registered on the shared ledger, it becomes permanent — no alterations or manipulations are possible.

If a transaction is recorded incorrectly, the only remedy is to enter a new, correcting trade that stands alongside the original, with both being openly recorded and observable.

Smart Contracts

Imagine a digital contract that executes itself when certain conditions are met.

These smart contracts are protocols written into the blockchain that autonomously carry out transactions when predefined criteria have been satisfied without intermediaries.

Step-by-step breakdown of how a blockchain works

Transaction Initiation

A user initiates a transaction, which could involve cryptocurrency, contracts, records, or other information.

Block Creation

The transaction is then grouped with other trades to create a data block. This block contains information about the transaction, including the date, time, and transaction amount, as well as digital signatures of the parties involved.

Transaction Verification

Before a block can be added to the blockchain, the transaction must be verified by the network. This is done using a consensus mechanism like Proof of Work, Proof of Stake, etc., depending on the blockchain's protocol.

Block Hashing

Once a transaction is verified, the block is given a hash. A hash is a unique identifier generated by a mathematical algorithm that transforms digital information into a series of numerals and characters.

If any piece of the block's data is altered, the hash would likewise undergo a detectable transformation.

Adding to the Blockchain

After hashing, the block is added to the blockchain. This block, now with a unique hash and following a strict chronological order, is attached to the previous block of the chain, creating a chain of blocks in sequential order.

Transparency

The addition of the block is broadcasted to all network participants, updating their blockchain copies.

Completion

The transaction is complete, and the updated blockchain includes a transparent transaction record accessible by all network participants.

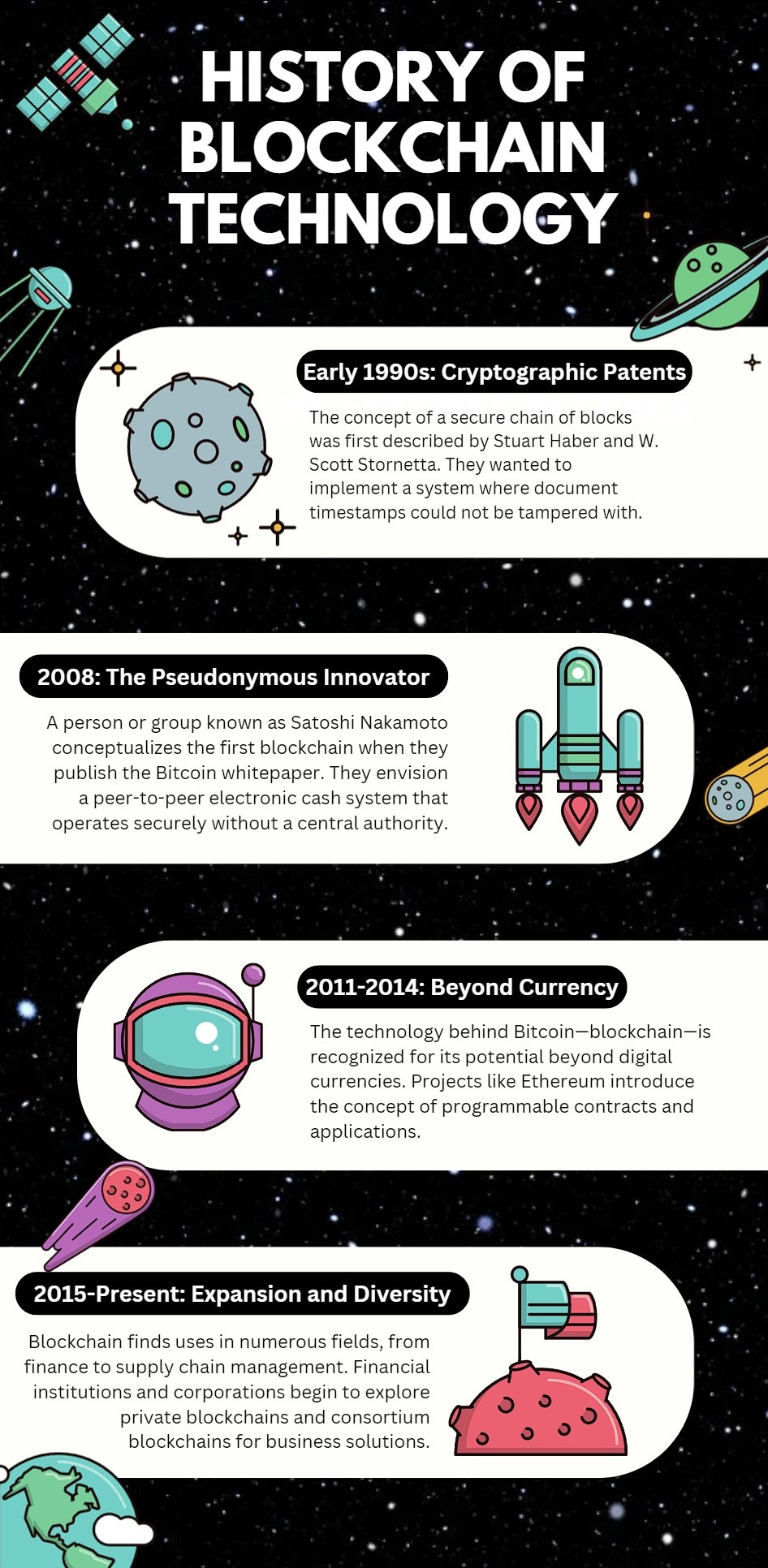

History of Blockchain Technology

The journey of blockchain technology began before it became the backbone of cryptocurrencies. It was conceptualized as a cryptographically secured chain of blocks by researchers Stuart Haber and W. Scott Stornetta in 1991.

Their initial work aimed to implement a system where document timestamps could be supported.

The Genesis of Bitcoin and Blockchain's Real-World Application

In 2008, the idea took a revolutionary turn with the advent of Bitcoin. An individual or collective using Satoshi Nakamoto's alias unveiled Bitcoin as a "peer-to-peer electronic cash system."

This marked the inception of the first decentralized blockchain, which resolved the long-standing double-spend problem in digital currency systems without the need for any trusted authority or central server.

The Blockchain Expansion Beyond Cryptocurrency

Blockchain technology proved its mettle by powering Bitcoin, but its potential was seen to be far more expansive.

With the emergence of platforms like Ethereum, blockchain technology evolved to facilitate not only transactions but also "smart contracts" and decentralized applications (dApps), which have implications across various sectors such as finance, healthcare, and logistics.

What are the types of blockchain networks?

Blockchain networks come in several different types, each with its unique features and use cases.

Here are the primary types of blockchain networks:

Public Blockchains

Public blockchains are accessible to everyone, allowing any individual to participate in the network. The network typically has an incentivizing mechanism to encourage more participants to join.

Transactions are transparent, and anyone can verify them.

Examples include Bitcoin and Ethereum.

Characteristics:

- Fully decentralized.

- No access restrictions.

- Typically, Proof of Work or Proof of Stake is a consensus mechanism.

Private Blockchains

A private blockchain is a closed network, typically managed by a single organization or entity. Participation is by invitation only, and permissions are restricted.

It's usually faster and more efficient than a public blockchain because it's smaller, and consensus can be reached more quickly.

Characteristics:

- Partially decentralized.

- Access is restricted to specific users.

- Faster transaction speeds due to a smaller number of nodes.

Consortium Blockchains

Consortium blockchains are semi-decentralized and allow multiple organizations to manage a single blockchain network. Control is shared equally among predetermined organizations, which leads to a higher level of trust among participants compared to public blockchains.

Characteristics:

- Decentralized to the extent of the consortium's members.

- It is not open to the public, but more than one organization controls the network.

- Often faster than public networks while maintaining higher security than private blockchains.

Hybrid Blockchains

Hybrid blockchains combine elements of both private and public blockchains. They allow control over who can access specific data on the blockchain and what transactions are made public. This type of blockchain aims to offer a balanced approach that provides the benefits of both types without the full exposure of public blockchains or the single point of control in private blockchains.

Characteristics:

- Controlled access and freedom at the same time.

- Users can decide what data is made public and what remains private.

- Offers flexible control over the blockchain.

Sidechains

Sidechains are blockchain networks that run parallel to a primary blockchain. Assets can be transferred between the primary chain and the sidechain, which allows for increased scalability and efficiency. Sidechains operate independently, with their own consensus algorithms and block parameters.

Characteristics:

- Operate independently from the main chain but are connected to it.

- It can have different security protocols or consensus mechanisms than the main chain.

- Allows for experimentation without impacting the main blockchain.

Permissioned (or Private) Blockchains

Permissioned blockchains are a variation of private blockchains where access to the network is controlled but might have a level of decentralization if managed by multiple organizations. They are often used in business-to-business scenarios.

Characteristics:

- Controlled access and permissions with multiple layers.

- Often used in enterprise environments for business collaboration.

Each type of blockchain network has specific applications and use cases, depending on the requirements for privacy, trust, throughput, and access control. Enterprises and individuals can choose the appropriate type of blockchain-based on their needs for scalability, control, and decentralization.

What are the benefits of blockchain technology?

Blockchain technology offers several key benefits that are driving its adoption across various industries:

Enhanced Security

Blockchain's use of advanced cryptography makes it highly secure. Each transaction is secured with encryption and connected to the preceding transaction. Additionally, because the information is stored across a network of computers, it is very resistant to hacking, as there is no single point of failure.

Increased Transparency

Because the blockchain ledger is decentralized, all participants on the network have access to a shared ledger rather than having separate individual copies.

Collective ledger can only be amended through consensus, meaning that any updates require universal agreement among the participants.

As a result, data on the blockchain is more accurate, consistent, and transparent.

Improved Traceability

In blockchain technology, whenever a transaction involving goods is recorded, it creates an audit trail that allows for the tracking of the goods' origin.

This feature of blockchain can be especially beneficial in sectors such as supply chain management, as it enhances the traceability of goods, prevents fraud, and ensures the authenticity of the products.

Reduced Costs

Blockchain reduces the reliance on third parties or intermediaries to guarantee transactions. The trust is shifted from the trading parties to the blockchain's data integrity.

This can significantly reduce costs by eliminating the need for various intermediaries.

Faster Transactions

Traditional banking systems can be slow, and cross-border transactions can take days to settle. Blockchains can process transactions more quickly because they don't require the lengthy process of verification, settlement, and clearance. After all, a single version of the truth is already available on a shared ledger.

Decentralization

Blockchain enables a decentralized approach to management and operations. Information is not stored in a central location but is accessible to all network participants.

This decentralization means no single entity has control over the entire network, which can reduce the likelihood of systemic failures and data tampering.

Automation Capability

Blockchain technology authorizes smart contracts development that automatically executes transactions when certain conditions are met. This automation can save time and effort while also ensuring the tasks are completed promptly and accurately.

Immutability

Immutability in blockchain ensures that once a transaction is recorded, it cannot be altered or deleted. This is crucial for audit purposes and gives a high degree of integrity to the data as a definitive record of events.

These benefits propel blockchain beyond its original application in cryptocurrency into fields like supply chain management, healthcare, finance, and real estate, among others.

What industries use blockchain?

As we mentioned before, blockchain can be used across a wide range of industries, revolutionizing how they operate by enhancing efficiency, security, and trust.

Here is a list of such industries:

Finance and Banking

Blockchain is perhaps most famously used in the financial sector for cryptocurrencies like Bitcoin. However, its applications are much broader, including facilitating cross-border payments, enabling real-time settlement systems, and ensuring compliance through transparent record-keeping.

Supply Chain Management

Companies use blockchain to create a transparent, tamper-proof record of the movement of goods. This visibility helps to ensure authenticity, prevent fraud, and reduce delays in shipment and delivery.

Healthcare

Patient records can be encrypted and stored on blockchain, providing a secure and immutable history of individuals' health data. This ensures privacy and enables healthcare providers to access a patient's history quickly and accurately.

Real Estate

Blockchain can streamline property transactions by securely recording, storing, and transferring real estate deeds and titles. This reduces fraud, eliminates paperwork, and simplifies the process.

Voting Systems

By offering a protected and transparent setting for casting, recording, and counting votes, blockchain can potentially eliminate election fraud and increase voter turnout.

Intellectual Property and Royalties

Artists, musicians, and authors can use blockchain to assert ownership over their intellectual property and automate royalty payments through smart contracts.

Energy Sector

Blockchain helps to efficiently track and manage energy distribution, often in projects involving peer-to-peer energy trading and renewable energy sources.

Legal Industry

Blockchain-based smart contracts can streamline the execution and fulfillment of contractual terms, diminishing the necessity for intermediaries like legal practitioners and escrow services.

Retail and E-commerce

It's used to verify the authenticity of products, manage supply chains, and prevent counterfeit goods from infiltrating the market. Additionally, blockchain-based cryptocurrencies are increasingly accepted as a form of payment.

Education

Academic credentials can be verified and stored on a blockchain, making it easier for employers to validate the educational background of potential employees.

Automotive Industry

Automakers are exploring blockchain for use cases ranging from supply chain tracking to the secure sharing of vehicle data for connected cars and autonomous vehicles.

Agriculture

Farmers can use blockchain to track the production, storage, and transportation of agricultural products, ensuring food safety and building trust with consumers.

The adoption of blockchain across these industries is still at various stages.

Still, the common thread is the pursuit of increased trust, accountability, and efficiency in transactions and record-keeping. The potential of blockchain is vast, and as it evolves, it is expected to permeate even more aspects of business and everyday life.

How does business and everyday life take advantage of blockchain?

Blockchain technology gives a lot of benefits for both businesses and everyday life, reshaping how we conduct transactions, establish trust, and exchange information.

Here are some key advantages:

Key advantages for businesses:

Improved Transparency

The distributed ledger of blockchain ensures that all participants on the network have access to common documentation, eliminating disparate individual copies. This unified record can only be updated through a consensus process, requiring all parties to be in agreement. As a result, the data on a blockchain is more precise, uniform, and transparent.

Enhanced Security

Before being recorded, transactions require consensus. Once approved, they are encrypted and connected to the preceding transaction.

This, coupled with the decentralized nature of storing information across a network of computers rather than a solitary server, significantly hampers a hacker's ability to manipulate transaction data.

Reduced Costs

For many businesses, reducing costs is a priority. Blockchain can help to cut costs by removing the go-betweens or third parties in many processes. For example, for payments, instead of paying a bank to validate a transaction, you can use blockchain to validate transactions yourself.

Increased Efficiency and Speed

Blockchain streamlines traditional, cumbersome paper-based processes that are slow, susceptible to human error, and frequently dependent on third-party mediation.

Transactions can be executed more swiftly and effectively because record-keeping is managed through a single digital ledger shared among all participants, eliminating the need for multiple ledgers and resulting in a more organized system.

Streamlined Supply Chains

Blockchain offers a precise and traceable ledger for every product, streamlining supply chain processes, curbing losses from counterfeit goods and unauthorized sellers, increasing transparency and adherence to regulations in outsourced manufacturing, and possibly elevating a company's stature as a frontrunner in ethical production practices.

Key advantages for everyday life:

Banking the Unbanked

Blockchain can provide secure and accessible financial services to those who are currently unbanked, which is nearly 1.7 billion people worldwide, according to the World Bank.

This can open up opportunities for people to access loans, start businesses, or just safely store their money.

Secure Personal Information

Blockchain could provide a higher standard of security for personal data. Social Security numbers, birth dates, and other personal data are less exposed to hacks.

Ownership of Digital Assets

Blockchain enables the use of smart contracts, which could revolutionize the management of ownership rights for digital assets like music, art, eBooks, and more, ensuring creators are paid fairly.

Voting Mechanisms

Blockchain can be used to create tamper-proof voting systems, which could lead to more secure, transparent, and accessible elections, potentially increasing voter turnout and trust in the electoral process.

Healthcare Records

Blockchain allows for medical records to be encrypted and recorded on the network, with access controlled by a private key, which ensures that only authorized individuals can view the information, maintaining confidentiality.

This can improve and simplify secure access to medical records for patients and healthcare providers alike.

Real Estate Processing

Blockchain could speed up home and real estate title transfers by securely verifying and storing documents, reducing fraud, and providing transparency throughout the entire process.

As blockchain technology progresses and becomes increasingly advanced mainstream, its applications will likely continue to grow, potentially transforming every major industry and impacting our daily lives in myriad ways.

The key to its widespread adoption will be ease of use for consumers and the ability to integrate with existing technologies.

Future Outlook

As we peer into the horizon of technological advancement, blockchain stands as a beacon of transformative potential. The technology is not static; it is rapidly evolving, addressing its current limitations and expanding its capabilities.

Innovations on the blockchain front are geared towards scalability, efficiency, and interoperability, among other aspects.

One of the foremost hurdles blockchain technology encounters is its ability to scale effectively and maintain scalability, with networks like Bitcoin and Ethereum seeking solutions to accommodate more transactions without compromising security or decentralization.

Innovations such as sharding, where the database is partitioned to spread the load, and layer-two protocols, which process transactions off the main chain, are in the pipeline.

Ethereum's transition to a proof-of-stake consensus mechanism through its Ethereum 2.0 upgrade is an example of the effort to increase transaction throughput while reducing energy consumption.

Interoperability is another frontier—different blockchain networks operating in silos restrict the seamless exchange of information and value.

Projects are underway to create protocols that enable blockchains to communicate with each other, effectively creating a network of chains that can transfer data and assets freely and securely.

The convergence of blockchain with other sophisticated technologies like Artificial Intelligence (AI) and the Internet of Things (IoT) heralds the dawn of enhanced performance and expanded possibilities.

AI can enhance the smart contract logic, security, and administrative operations of blockchain networks. At the same time, IoT devices can leverage blockchain for secure, autonomous transactions and data exchanges.

As blockchain matures, we can anticipate its footprint to expand into areas not traditionally associated with technology. The fusion of blockchain with these emergent technologies promises a future where digital and physical worlds converge in a secure, decentralized, and efficient manner.

Overall Conclusion

In conclusion, blockchain technology is much more than a platform for cryptocurrencies. It's a revolutionary system that provides security, transparency, and efficiency with various applications across various sectors.

From supply chain management and healthcare to banking and real estate, the implications of blockchain are widespread, influencing both the macro structures of global industries and the micro aspects of daily living.

As we continue to witness the convergence of blockchain with other transformative technologies, its full potential is yet to be realized.

The future promises greater scalability, interoperability, and integration, which will likely foster new use cases and solutions to complex problems.

While blockchain is a powerful tool, it is not a panacea. Challenges such as regulatory hurdles, environmental concerns, and the need for better user interfaces must be addressed to realize its full potential.

Nonetheless, as technological literacy grows and development continues, blockchain is poised to become an integral part of our digital infrastructure.

Businesses and individuals alike stand to gain from embracing blockchain, whether it's through increased operational efficiency, enhanced security measures, or simply by having more control over one's data and assets.

As the world grows increasingly interconnected and digitalized, blockchain technology may be the backbone of a new era of innovation and trust in the digital landscape.